Market valuation hits $36 billion

The real-world asset (RWA) tokenization market has crossed a significant threshold, with total value exceeding $36 billion as of late 2025. This figure, excluding stablecoins, marks a decisive shift from experimental pilot programs to a substantive asset class. According to the Canton Network’s State of RWA Tokenization 2026 report, this growth reflects a broader institutional acceptance of blockchain-based settlement for traditional finance.

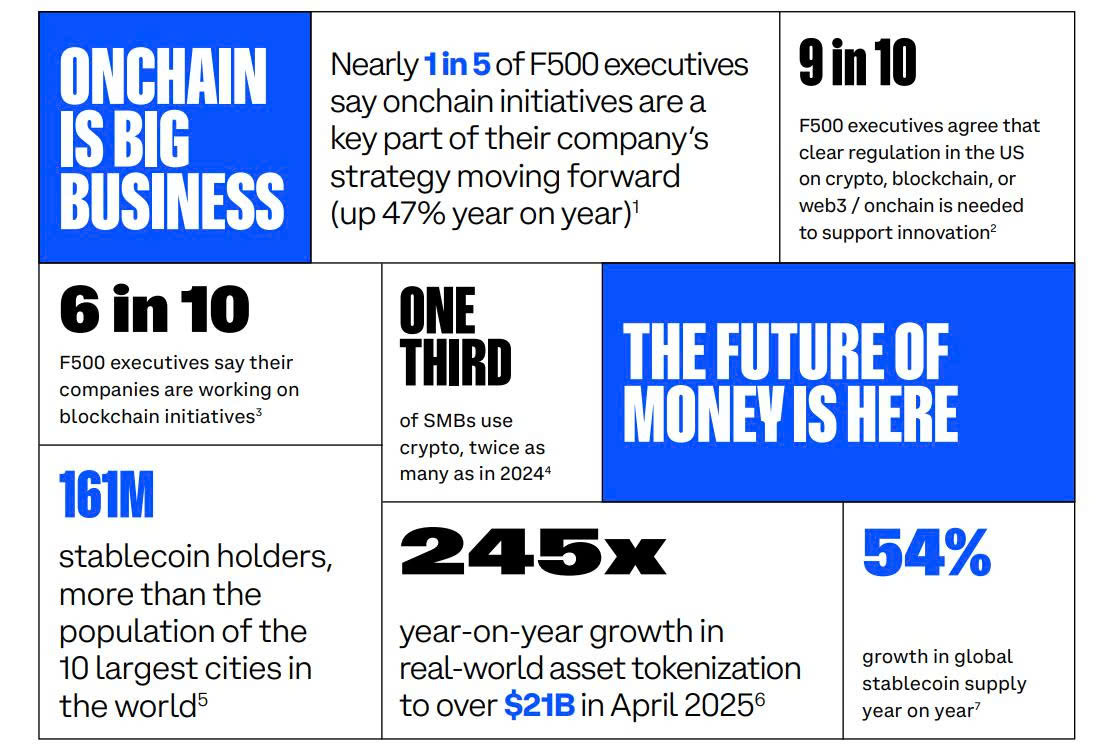

The trajectory has been steep. Data from RWA.xyz indicates that tokenized RWAs grew by 266% in 2025, reaching over $24 billion in total value by February 2026. While different methodologies may yield slightly higher or lower totals, the consensus is clear: the sector is scaling rapidly. This expansion is driven largely by the tokenization of treasury bills, private credit, and real estate, which offer yield and liquidity advantages that traditional markets struggle to match.

However, this growth is not uniform. The market remains fragmented across multiple blockchains, leading to liquidity silos. As capital flows into tokenized assets, the challenge for issuers and investors alike is navigating this fragmented landscape to ensure efficient price discovery and settlement. The current valuation suggests that RWA tokenization is no longer a niche experiment but a core component of the evolving digital asset ecosystem.

Tokenized treasuries lead the charge

Tokenized U.S. Treasuries have emerged as the dominant category in the real-world asset (RWA) market, accounting for the largest share of on-chain fixed-income value. By early 2026, the market for tokenized Treasuries had surpassed $12.8 billion, driven by institutional demand for yield that traditional banking systems struggle to match. This segment acts as the foundational liquidity layer for DeFi, bridging the gap between regulated money markets and decentralized protocols.

The appeal lies in the yield differential. While traditional money market funds often lag behind federal funds rates due to fees and operational friction, tokenized Treasuries offer near-real-time access to the full risk-free rate. Protocols like Ondo Finance and Franklin Templeton’s Benji have capitalized on this by allowing investors to hold tokenized versions of short-term government debt directly in their wallets. This structure reduces settlement times from days to seconds and eliminates many intermediary costs.

This efficiency has attracted significant institutional capital. Major financial players are no longer experimenting with the technology; they are integrating it into core treasury management strategies. The ability to programmatically manage collateral and access instant liquidity makes tokenized Treasuries a superior alternative to traditional bank deposits for many corporate and institutional treasuries.

Institutional demand drives liquidity

Traditional finance institutions are moving from pilot programs to active deployment, treating real-world asset (RWA) tokenization not as an experiment but as a necessary infrastructure upgrade. The primary driver is liquidity. By tokenizing illiquid assets like private credit or real estate, institutions can unlock capital that was previously trapped in long settlement cycles. This shift requires deep integration with decentralized finance (DeFi) protocols, but only under strict compliance frameworks.

The gap between traditional settlement and blockchain speed is the most immediate value proposition. Traditional markets operate on T+2 settlement, meaning trades take two days to clear. RWA tokenization enables T+0 settlement, allowing for instant finality. This speed reduces counterparty risk and frees up capital for reinvestment. The following comparison highlights the operational differences institutions are navigating.

| Feature | Traditional Finance | RWA Tokenization |

|---|---|---|

| Settlement Time | T+2 days | T+0 (Instant) |

| Intermediaries | Multiple (Banks, Clearing Houses) | Smart Contracts (Automated) |

| Accessibility | Institutional Only | Permissioned Retail & Institutional |

| Cost Structure | High (Manual Processing) | Lower (Automated Execution) |

Compliance and Know Your Customer (KYC) integration are non-negotiable for institutional entry. Unlike public DeFi, institutional RWA platforms require embedded identity verification. This means KYC checks are baked into the token standard itself, ensuring that only verified participants can hold or trade these assets. This approach satisfies regulatory requirements while maintaining the efficiency benefits of blockchain technology. Without this layer, institutions cannot deploy significant capital due to legal and audit constraints.

Fragmentation remains a hurdle. As of late 2025, the tokenized RWA market exceeded $36 billion, excluding stablecoins, but liquidity is scattered across multiple chains and platforms [src-serp-1]. Institutions need deeper, consolidated liquidity pools to execute large trades without significant slippage. The next phase of adoption will likely involve cross-chain interoperability solutions that allow institutions to access unified liquidity while maintaining their specific compliance standards.

Fragmentation Challenges in RWA Tokenization

The RWA tokenization market exceeded $36 billion in late 2025, yet this growth is masked by a critical structural flaw: fragmentation. Tokenized assets are siloed across disparate blockchains, creating liquidity islands that prevent the unified market necessary for mass institutional adoption. Without interoperability, a tokenized bond on one chain cannot easily interact with a lending protocol on another, severely limiting utility and price discovery.

Cross-chain interoperability remains the primary technical hurdle. Current solutions often rely on bridges that introduce latency and security risks, or they require complex wrapping mechanisms that obscure the underlying asset. This lack of seamless connectivity means that even as the total value of tokenized real-world assets grows, the effective liquidity available to traders and institutions remains artificially constrained. The market is large, but it is not liquid in a meaningful, unified sense.

Regulatory fragmentation compounds the technical issues. Different jurisdictions enforce varying standards for asset custody, proof of reserve, and investor eligibility. A tokenized real estate fund compliant in Singapore may face immediate barriers in the European Union due to differing MiCA interpretations. This regulatory patchwork forces issuers to build isolated compliance frameworks for each chain and jurisdiction, further deepening the fragmentation.

Until a unified standard emerges—whether through a dominant Layer 1, a cross-chain messaging protocol, or a regulatory harmonization framework—the RWA tokenization market will remain a collection of isolated experiments rather than a cohesive financial infrastructure. Investors and institutions must navigate this complexity carefully, recognizing that the headline market size figures do not reflect the actual tradable liquidity available.

Key questions on RWA adoption

What is the state of RWA tokenization in 2026?

Market data shows how concentrated tokenized RWAs remain. According to RWA.xyz, tokenized RWAs grew to over $24 billion in total value by February 2026, with a 266% growth in 2025. Other data sources, like RWA.io, may place the figure even higher, depending on methodology.

Is RWA tokenization the future?

The future of RWA looks extremely promising. Expected to reach trillions in market size by 2030, integration with DeFi protocols will deepen. Tokenized securities and funds will dominate, and more compliant and regulated platforms will emerge.

What are the main barriers to RWA adoption?

While the growth is significant, regulatory clarity remains a primary hurdle. Institutions require standardized legal frameworks to ensure that digital tokens representing real-world assets are enforceable across jurisdictions. Without these frameworks, widespread institutional adoption may remain cautious despite the technological potential.

No comments yet. Be the first to share your thoughts!