Market size and growth drivers

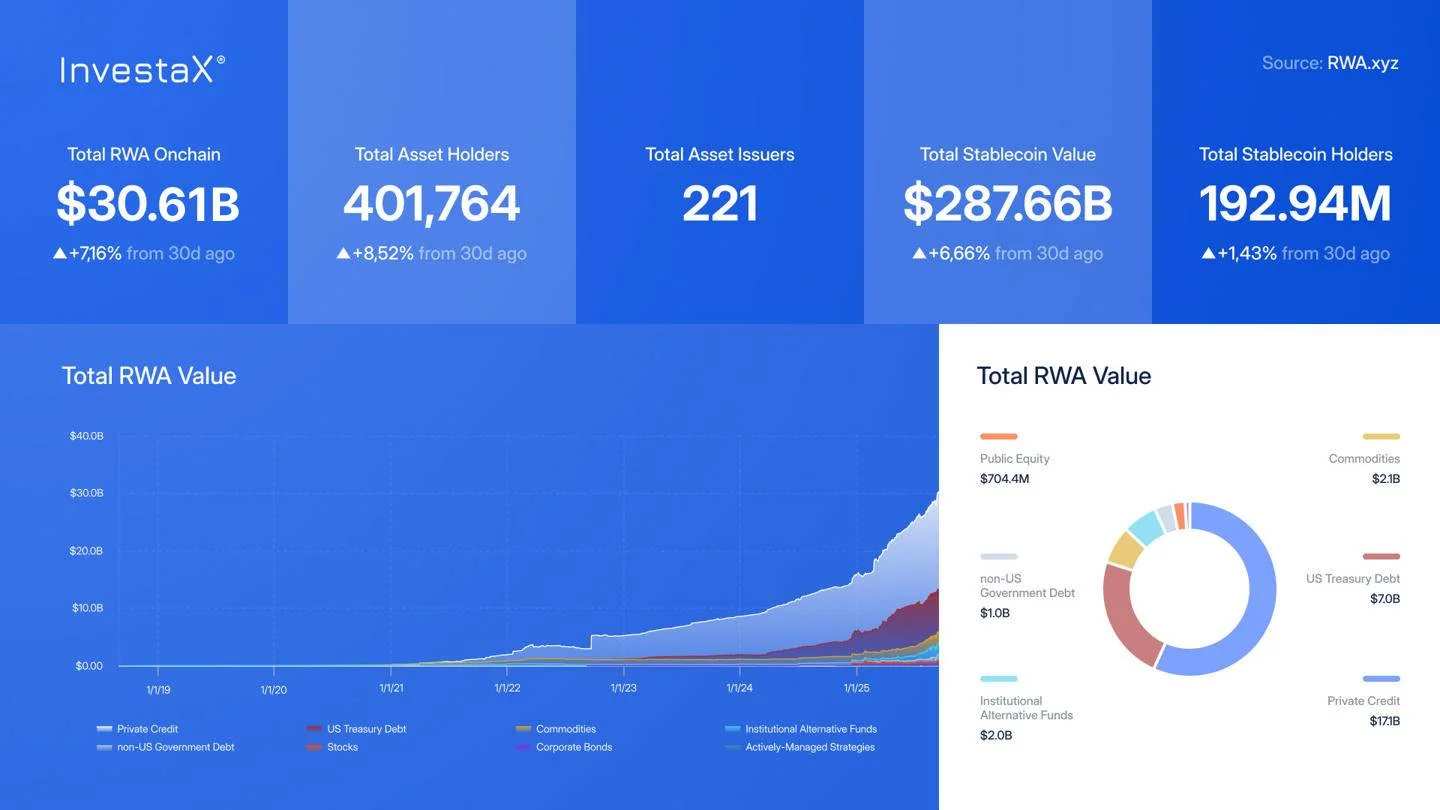

The real-world asset (RWA) tokenization market has moved beyond experimental phases into a phase of substantial institutional scale. As of late 2025, the total value of tokenized assets excluding stablecoins surpassed $36 billion, according to data from Canton Network’s annual report. This milestone reflects a structural shift in how traditional finance institutions approach liquidity and settlement, driven by the need for more efficient capital markets infrastructure.

While some earlier metrics from early 2026 placed the broader RWA market at approximately $24 billion, the divergence in valuation methods highlights the rapid maturation of the sector. The 266% growth recorded in 2025 alone indicates that institutional demand is no longer speculative but operational. Companies like Securitize and Brickken are central to this expansion, providing the necessary compliance and custody layers that allow traditional assets to enter the blockchain ecosystem without compromising regulatory standards.

The primary drivers behind this growth are regulatory clarity and institutional efficiency. As frameworks in the EU (MiCA) and the US evolve, the friction associated with cross-border asset transfers decreases. This environment allows tokenized treasuries, private credit, and real estate to trade with greater speed and lower counterparty risk. The fragmentation across multiple blockchains remains a challenge, but the capital influx suggests that interoperability solutions are becoming a priority for major market participants rather than an afterthought.

Top RWA tokenization platforms

The real-world asset (RWA) tokenization market has matured into a structured infrastructure layer for institutional finance. In 2026, the $36 billion market is no longer defined by experimental pilots but by established platforms that handle compliance, custody, and secondary trading for specific asset classes. Choosing the right platform is a critical decision, as each provider has carved out distinct niches ranging from private credit to tokenized treasuries.

The following comparison highlights the leading infrastructure providers shaping the 2026 landscape. These platforms are selected based on their institutional adoption, regulatory compliance frameworks, and specific focus areas.

| Platform | Primary Focus | Underlying Tech | Key Feature |

|---|---|---|---|

| Securitize | Treasuries & Private Credit | Multichain (Ethereum, Polygon) | Fully compliant security token issuance and transfer agent services |

| Brickken | Real Estate & SME Equity | Ethereum & Polygon | Fractionalized ownership with integrated KYC/AML for retail and pro investors |

| Centrifuge | Real World Assets (DeFi Integration) | Ethereum (via Arbitrum) | Direct integration with Aave and other DeFi lending protocols for asset-backed liquidity |

| Ondo Finance | Tokenized Treasuries & Bonds | Ethereum & Avalanche | High-yield tokenized US Treasury products (e.g., OUSG) with institutional-grade custody |

| Tokeny | Corporate Bonds & Funds | Ethereum, Polygon, BNB Chain | Strong focus on European MiCA compliance and transfer agent capabilities |

Securitize remains the dominant infrastructure provider for large-scale security token issuance. Its multichain approach allows issuers to deploy tokens on Ethereum or Polygon while maintaining rigorous transfer agent compliance. For institutions issuing tokenized treasuries or private credit funds, Securitize provides the necessary regulatory backbone.

Brickken has positioned itself as the go-to platform for real estate and small-to-medium enterprise (SME) equity. By combining fractionalization technology with built-in compliance tools, it lowers the barrier to entry for accredited and non-accredited investors alike, making it a key player in democratizing access to alternative assets.

Centrifuge bridges the gap between traditional finance and decentralized finance (DeFi). It allows real-world assets like invoices or real estate to be used as collateral in DeFi protocols like Aave. This unique model provides liquidity to asset owners who might otherwise be locked out of traditional lending markets.

Ondo Finance specializes in tokenized U.S. Treasuries and short-term bonds. Its products, such as OUSG, offer institutional-grade custody and yield, attracting capital from both traditional finance and crypto-native investors seeking stable, on-chain returns.

Tokeny focuses heavily on the European market, ensuring its platforms are fully compliant with the Markets in Crypto-Assets (MiCA) regulation. It is particularly strong in the issuance of tokenized corporate bonds and investment funds, providing robust transfer agent services for European issuers.

As an Amazon Associate, we may earn from qualifying purchases.

Tokenized treasuries lead adoption

Tokenized US Treasuries have emerged as the dominant category in the $36 billion real-world asset (RWA) market. With a market capitalization of $12.88 billion, this segment accounts for a significant portion of on-chain fixed-income activity. The growth is driven by institutional demand for accessible, on-chain yield that bypasses traditional settlement delays.

Securitize provides the infrastructure for regulated token issuance, enabling institutions to hold US Treasuries directly on-chain. Brickken focuses on fractionalization and secondary liquidity, allowing high-net-worth individuals and funds to trade treasury shares with greater ease than conventional bond markets permit.

This shift reflects a broader move toward programmable finance. By tokenizing treasuries, institutions gain 24/7 settlement, reduced counterparty risk, and seamless integration with DeFi yield strategies. The result is a more efficient capital allocation mechanism that bridges traditional finance with decentralized infrastructure.

Institutional allocation shifts

The landscape of real-world asset (RWA) tokenization is no longer defined by speculative experiments but by deliberate portfolio construction. By 2026, high-net-worth individuals are projected to allocate 8.6% of their portfolios to tokenized assets, signaling a structural shift in how wealth is deployed across private markets [[src-serp-5]]. This is not a fleeting trend; it represents a maturation of the asset class as institutions seek liquidity and fractional ownership in traditionally illiquid sectors.

Institutional capital is following a similar trajectory, driven by the need for efficiency in private credit and real estate. The total value of tokenized assets has surpassed $36 billion, with significant volumes moving through regulated infrastructure [[src-serp-7]]. Securitize and Brickken have become critical intermediaries, providing the compliance and settlement layers that allow institutions to integrate these assets into existing custody and trading systems without operational friction.

The shift is particularly evident in private credit, where tokenization has unlocked over $12.88 billion in new capital flows [[src-serp-7]]. Institutions are using these platforms to bypass traditional intermediaries, reducing settlement times from days to minutes and lowering the cost of capital. This efficiency is driving the 8.6% HNW allocation figure, as wealthy investors gain access to institutional-grade deals previously reserved for large funds. The focus has moved from "if" to "how," with platforms competing on regulatory clarity and integration capabilities rather than just token volume.

Fragmentation and interoperability

The tokenized RWA market exceeded $36 billion by late 2025, yet this growth is constrained by a fractured infrastructure. Assets are currently siloed across isolated blockchains, forcing institutional players to maintain complex, redundant custody and compliance stacks for each ledger. This fragmentation prevents the formation of a single, liquid global market for real-world assets.

Leading platforms are now prioritizing interoperability to bridge these divides. Securitize has expanded its cross-chain capabilities, allowing asset managers to deploy tokenized funds on multiple networks without rebuilding their underlying infrastructure. Similarly, Brickken’s modular architecture enables seamless asset migration, reducing the operational friction that previously deterred large-scale institutional adoption.

As these protocols mature, the industry is shifting from isolated pilot programs to interconnected ecosystems. This move toward a unified market is essential for unlocking the full liquidity potential of the $36 billion RWA sector, ensuring that tokenized assets can move as freely as traditional securities.

No comments yet. Be the first to share your thoughts!