RWA tokenization market size and growth trajectory

The RWA tokenization market has moved decisively past the experimental phase into institutional-scale deployment. By early 2026, the total value of tokenized real-world assets exceeded $24 billion, with some estimates placing the broader market—excluding stablecoins—above $36 billion as of late 2025. This rapid expansion reflects a structural shift in how capital markets interact with decentralized finance, driven by regulatory clarity and the entry of major financial infrastructure providers.

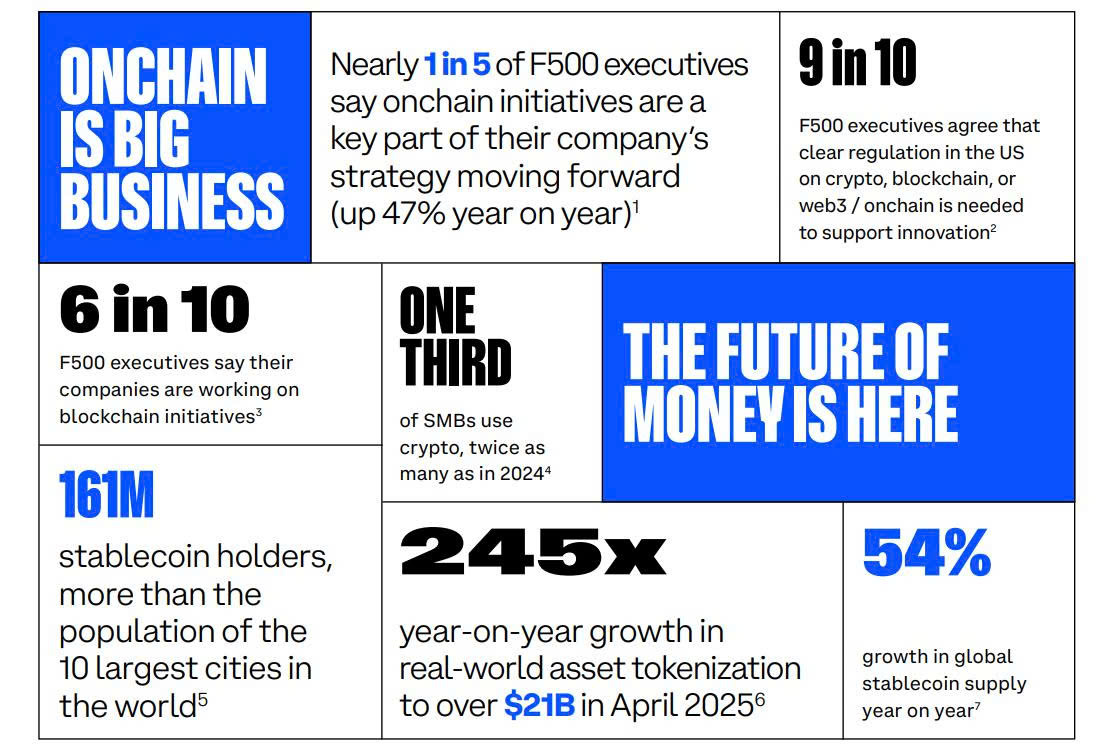

Growth has been particularly sharp in 2025, where the sector recorded a 266% year-over-year increase in total value locked. While broader market reports project the tokenization segment to reach $5.19 billion in 2026 at a 26.4% CAGR, these figures often focus on specific verticals or exclude the wider ecosystem of tokenized treasuries and private credit. The divergence in data sources highlights the current fragmentation across chains, yet the underlying trend remains unequivocally upward.

This trajectory signals that RWA tokenization is no longer a niche experiment but a core component of the digital asset landscape. Institutional capital is increasingly flowing into these tokenized instruments, seeking the liquidity and efficiency that blockchain infrastructure provides. As the market matures, the focus is shifting from mere adoption to interoperability and standardized compliance frameworks.

Institutional Drivers Reshaping Liquidity

The entry of major financial institutions into the tokenization space in 2026 is no longer speculative; it is a structural response to three converging pressures: regulatory clarity, yield scarcity in a high-rate environment, and the demand for efficient settlement. Unlike the experimental phases of previous years, current institutional adoption is driven by tangible balance sheet benefits and compliance-ready infrastructure.

Regulatory Clarity as a Foundation

The primary catalyst for institutional entry is the maturation of regulatory frameworks. In 2026, jurisdictions with clear guidelines on asset custody, smart contract liability, and investor protection have become the preferred hubs for tokenized assets. This clarity reduces legal overhead and allows traditional banks to treat tokenized securities with the same rigor as traditional bonds or equities. Without this regulatory certainty, institutional capital would remain on the sidelines due to compliance risks.

Yield Seeking in a High-Rate Environment

In an environment where interest rates remain elevated, institutions are actively seeking yield that outperforms traditional fixed-income instruments. Tokenized money market funds and short-term government bonds offer higher efficiency and accessibility. By tokenizing these assets, institutions can access 24/7 liquidity and fractional ownership, appealing to a broader range of investors while maintaining the stability of underlying real-world assets. This demand is particularly strong among asset managers looking to optimize portfolio returns without taking on excessive risk.

The Need for Efficient Settlement

Settlement efficiency is the operational driver behind institutional adoption. Traditional cross-border transactions can take days to settle, tying up capital and increasing counterparty risk. Tokenization enables near-instant settlement through distributed ledger technology, reducing the need for intermediaries and lowering transaction costs. This efficiency is critical for high-frequency trading and large-scale institutional operations, where time and cost savings translate directly to competitive advantage.

Platform and Chain Comparison

The RWA tokenization landscape in 2026 is defined by fragmentation. As the market exceeds $36 billion, distinct platforms and blockchains have emerged with specialized strengths in custody, compliance, and asset types. Selecting the right infrastructure depends on whether the priority is institutional regulatory adherence or DeFi composability.

The following table compares the primary ecosystems facilitating these transactions.

| Platform / Chain | Custody Model | Regulatory Focus | Primary Asset Classes |

|---|---|---|---|

| Ethereum | Institutional-grade (L2s) | Global, MiCA-ready | Treasury bills, private credit |

| XRP Ledger | Ripple Custody | Dubai Land Registry sync | Real estate, property deeds |

| Avalanche | Subnet-specific custodians | US-focused, SEC-aligned | Corporate bonds, funds |

| Canton Network | Privacy-preserving shards | Cross-border, GDPR | Interbank settlements, syndicated loans |

Ethereum remains the dominant settlement layer for high-value treasury bills and private credit, leveraging its robust Layer 2 ecosystem for lower fees. Meanwhile, the XRP Ledger has carved out a niche in real estate, particularly through partnerships with Dubai’s land registry, enabling title deed tokenization with direct legal sync. For institutional investors requiring strict US regulatory alignment, Avalanche’s subnet architecture offers customizable compliance boundaries. Canton Network addresses the cross-border friction of syndicated loans by using privacy-preserving shards, allowing banks to transact without exposing sensitive data publicly.

Fragmentation and interoperability hurdles

The tokenized RWA market exceeded $36 billion by late 2025, excluding stablecoins, yet this growth masks a critical structural weakness: liquidity remains trapped in silos. As capital flows into digital assets, the absence of seamless cross-chain communication means institutional-grade assets are often inaccessible to the broader DeFi ecosystem. This fragmentation dilutes depth, making large-scale transactions more expensive and prone to slippage.

Interoperability is no longer a technical luxury but a market necessity. Without standardized bridges and universal settlement layers, assets on one chain cannot easily serve as collateral on another. This disconnect prevents the creation of a unified liquidity pool, forcing institutions to navigate complex, fragmented on-ramps that increase operational risk. The 2026 landscape demands protocols that can move value and data securely across disparate networks without compromising compliance or security.

| Feature | Current State |

|---|---|

| Liquidity Depth | Fragmented across isolated chains |

| Cross-Chain Collateral | Limited by bridge reliability |

| Institutional Access | High friction due to siloed protocols |

Resolving these hurdles requires a shift toward interoperability standards that prioritize security over speed. Protocols that enable native cross-chain asset transfers will likely capture the majority of institutional volume, as they reduce counterparty risk and streamline settlement. The winners in 2026 will be those that build the plumbing for a truly liquid, borderless RWA market.

Key questions on RWA tokenization

The RWA tokenization market is expanding rapidly, with projections indicating growth from $4.1 billion in 2025 to $5.19 billion in 2026 at a 26.4% CAGR [src-serp-1]. By February 2026, total tokenized asset value surpassed $24 billion, reflecting a 266% year-over-year increase [src-serp-2]. This growth is driven by institutional demand for compliant, liquid alternatives to traditional capital markets, which could eventually tokenize over $100 trillion in global assets [src-serp-3].

No comments yet. Be the first to share your thoughts!